Bears Have Bulls On the Ropes – A Decline Today Would Deliver A Knockout!

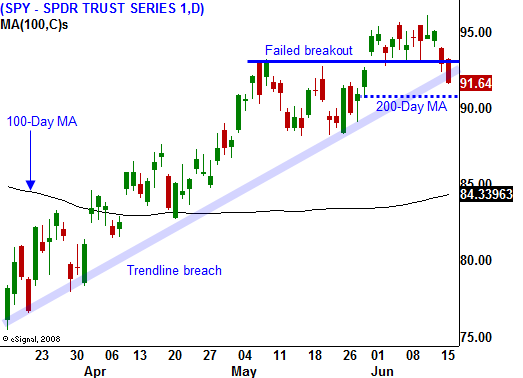

Wednesday 10:00 pm ET - Monday, the market started off on a weak note and it did not stage one of its typical late day rebounds. We finished below key support at SPY 93 and the bears were close to a breakdown. They just needed another decline to gererate additional selling pressure and they got it Tuesday.

There weren't any news events to justify Monday's decline and that strengthens my bearish sentiment. The market is tired after a 40% rebound from its March lows and it has run out of "drivers". Better than expected earnings and stability in the financial sector have run their course.

The headwinds are stiff. We are just above the 200-day moving average and that could fall today. We are right at a long-term downtrend and just above a short term up trend that started in March. If SPY 91 fails today, bears will take charge.

The most recent rally has been concentrated in a very narrow group of stocks (commodities and big-cap tech). That is not healthy for a sustained breakout. On a fundamental basis, we continue to see big job losses and interest rates are rising. 30-year mortgage rates have risen 1% in the last month and traders are hawking interest-rate yields. Every other week, the Treasury will hold bond auctions to raise more than $1 trillion this year. We made it through last week's auctions unscathed, but we have 3-year, 5-year and 7-year auctions next week. The bulls will continually be dodging bullets.

Yesterday, we saw a huge jump in housing starts. While that number seemed encouraging, it was primarily due to a spike in multi-family construction. That number was down huge in April and up huge in May. I believe this number was grossly understated in April and as a result we are seeing a big rebound. That suspicion was confirmed this morning when mortgage applications dropped 17% in the last week. Housing is weak and it will continue to be weak as tight credit and rising interest rates take their toll.

The Producer Price Index came in better than expected yesterday and inflation does not seem to be an issue. The CPI came in better than expected this morning and it only rose .1%. This is good news since consumers are getting hit from all other sides.

Gasoline prices are on the rise, lines of credit have been reduced, interest rates are on the rise, taxes are going higher (federal, state and municipal) and wages are declining. These are all chipping away at our purchasing power. Consumption makes up 70% of our GDP and without it, an economic recovery won't materialize.morning.

Bank of America announced that its credit card default rate rose to 12.5% in the last month. That is a 2% jump from 10.5% in April. A month ago, they predicted that their credit card default rate could rise to 24% before this economic cycle runs its course.

This morning FedEX released earnings and they are viewed as an economic barameter. They gave very dismal guidance and the market declined on the news. Looking ahead, "the operating environment for our first two quarters in fiscal 2010 is expected to be extremely difficult," said CFO Alan Graf.

I can see cracks in the dam and we are about to see a market decline. The VIX spiked yesterday and uncertainty is on the rise.

The A/D is a negative 1:2 and I believe we are headed lower today. If we get selling into the bell, add to short positions. Defense stocks, restautrants and REITS are weak. I will not short commodities since I like them long term, but they are weak.

Daily Bulletin Continues...