Actions – Not Words. Our Foreign Lenders Might Be Forcing Us To Abandon QE2

After making a new two-year high, the market is consolidating. Since the beginning of September, stocks have run up 16%. The news has been positive, but it was already priced in.

Republicans won the elections and they promise to trim deficit spending. Unfortunately, entitlement is source of the problem and newly elected officials won't commit political suicide by initiating Social Security/Medicare reform. President Obama suggested that the Bush tax credits might be extended for all Americans and that was the catalyst for last week's rally.

The Fed announced a $600 billion quantitative easing program. That was largely in line with expectations and it did not spark a rally. QE2 is an act of desperation and the US is losing credibility during this week's G20 meeting in South Korea. We accused China of currency manipulation and here we are printing money. The entire maneuver is likely to add less than .2% to our GDP.

As the dollar declines, it will become more expensive for the US to import goods. We have a massive trade deficit and this will result in inflation. Nations around the world want to keep their currencies "cheap" and QE2 could start a vicious devaluation cycle. China and Japan have the power to end this and they don't need to say one word.

China has massive foreign reserves ($2.5 trillion) and they are spending this "funny money" on hard assets. They have been passive in our bond auctions because they already own 5% of our debt. Japan owns another 5% of our debt. Both countries are criticizing the US for QE2 and all they need to do is to sell a small portion of their U.S. Treasuries to make a point. That would send interest rates higher and quantitative easing would be rendered useless.

Since the Fed announced its plan, interest rates have been creeping higher. We have mountains of debt to finance and every other week we hold huge bond auctions. Almost half of our national debt is held by foreigners and we need them to buy our bonds so that we can continue our gluttonous lifestyle. If our two largest lenders decide to become net sellers of our debt, interest rates will spike and the Fed will need to quickly abandon quantitative easing. They know this risk exists and that is why they chose to gradually test the water.

Credit concerns in Europe are flaring up again. Interest rates in Portugal, Ireland and Greece (PIG) jumped higher this week. Auctions did not go well in Portugal and Greece is running a much bigger deficit than projected. Germany is pushing for reform and it wants to realign the risk associated with potential EU bailouts. In short, they don't want to take the fall for everyone else's reckless spending. As the largest EU member, they are the kingpin. "Little ole Greece" was easy enough to backstop, but other nations are starting to line up for aid. Structural reform to pension benefits is needed. Without it, deficits will climb and a financial crisis will rip the EU apart.

Unfortunately, we are faced with a similar situation. Credit concerns in Europe could easily spread to the US. Our own credit crisis could unfold internally as states go bankrupt.

These credit issues won't go away. They will continue to smolder until they ignite. Deficit spending can go on for years until a "flash point" is reached. An aging population will quickly push the EU and the US to the brink of disaster and we are not more than a year or two from a crisis that will make 2008-2009 look like a cake walk. Investors are already losing faith in foreign currencies and the demand for gold is rising.

From a trading standpoint, we need to keep a close eye on interest rates (particularly in the US and Europe). Any rise that is not accompanied by economic growth will be tied to inflation or credit risk.

Next week, the economic news is fairly light. We will get PPI and CPI. I am expecting to see wholesale prices move higher, but consumer prices are likely to be benign. Weak demand will keep producers from raising prices and that means profit margins will start to decline. This will not be a major market mover and investors will focus on improving employment. Last week, private sector job growth increased for the 4th straight month and yesterday’s initial jobless claims were much better than expected. ISM services and manufacturing were also strong last week.

The market needs time to consolidate. It will gather strength for a year-end rally and credit concerns are the perfect scapegoat for a brief pullback. Promises of a balanced budget and new austerity measures will calm nerves and the market will recover.

Corporate profits have been excellent and money will rotate out of bonds and into stocks. I advised you to take profits on long positions ahead of the elections and if you followed my advice, you are flat. The market has not gone anywhere and you can objectively evaluate the price action from the sidelines.

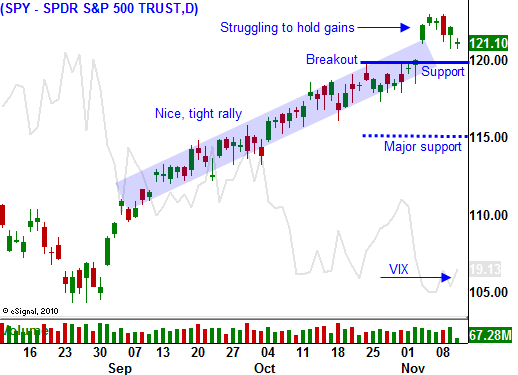

The market broke out above SPY 120 and that support level will be tested. If it holds, it is a sign that Asset Managers are aggressive and they want to get in. If it fails, bullish speculators will get flushed out and we will see a sharp, brief decline. Once support is established, I will be getting long. Companies that cater to emerging markets and generate most of their revenues overseas will be the focus. They can benefit from growth and they are hedged against a falling dollar. If we get a big pullback, I will buy calls. If the pullback is small (SPY 120) I will sell out of the money put spreads.

Be patient, wait for support and trade from the long side knowing that long term problems will fester and keep this market from getting ahead of itself. The rally will be very contained and orderly.

A spike in interest rates will force a big selloff in coming months and that is the warning sign to watch for.

THANK YOU TO ALL OF THE VETERANS WHO HAVE FOUGHT FOR FREEDOM AND WHO HAVE PRESERVED OUR WAY OF LIFE.

Daily Bulletin Continues...