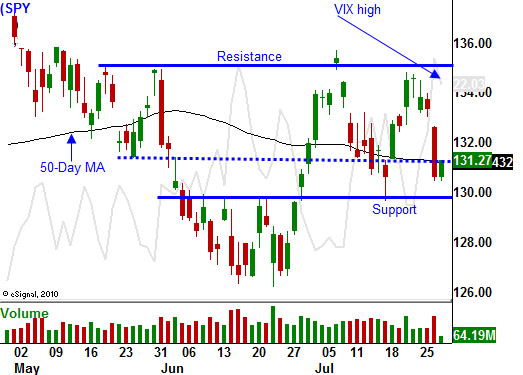

Traders Still Believe In A Weekend Deal – No Progress Would Spell Disaster For Stocks On Monday

Yesterday, stocks tumbled and issues other than the debt ceiling finally got the attention they deserve. Economic conditions are softening globally and interest rates are climbing in Spain and Italy. Politicians continue to sling mud during the debt ceiling crisis and investors are nervous.

I was amazed at how calm the market was on Monday when a debt ceiling deal had not been reached. That night, the President and the Speaker of the House publicly bashed each other. The exchange showed the world just how dysfunctional our government is on national TV. Republicans and Democrats are drafting their own plans and today the House will vote on Boehner's solution. Even if it passes the House, it needs 60 votes in the Senate and 53 members have already signed the document saying that they will not support it.

The clock is ticking and we don't have time to go back and forth between plans. At a time when the President should be mediating, he is taking sides. The debt ceiling will get raised, but it will not address structural issues. The "watered down" plan will lead to a credit downgrade. Republicans and Democrats are more distant than I can ever recall.

From a trading standpoint, here's how I see this playing out. The market will drift lower into the weekend, but we will avoid a meltdown. Traders still have faith that the deal will get done over the weekend and they don't want to be short if this happens. If we come in Monday morning without an agreement, the market will tank.

There will be chaos Sunday night when Asian markets open. China will release its PMI and it will fall below 50 (economic contraction). Traders are already prepared for this because of the "flash reading" last week, but this splash of cold water combined with our inability to reach an agreement will spark selling.

Monday morning, the S&P 500 could be down 20 points or more. A clear message will be sent to Washington and politicians will scramble to find middle ground. Once the debt ceiling is raised, we will get a relief rally. Almost every analyst on CNBC is calling for a rally once we put this behind us. They are calling for smooth sailing ahead, I disagree. The rally will be short-lived because of all of the other issues that are starting to surface.

Earnings have been fantastic. More than 80% of companies have exceeded estimates and the average" beat" is 15%. Stocks are undervalued, but there are a few things to keep in mind. Estimates have been lowered and companies should have been able meet or beat. Secondly, guidance has been cautious and many companies (CAT, UPS and MMM) see a slowdown ahead. Less than 10% of the companies that have reported have guided during this time of uncertainty. Even after posting excellent results, stocks are selling off. For eight straight quarters, stocks have declined after the first few weeks of earnings season.

Economic conditions in the US are deteriorating. Inventories have been rebuilt, $800 billion in fiscal stimulus has been spent and QE2 has ended. Even with all of these "drivers", we were only able to muster a few months of private-sector job growth. Tomorrow, analysts are expecting a meager 1.8% GDP growth rate. According to most economists, our activity was supposed to be clipping along by now. On a real basis (inflation-adjusted), our economy is contracting.

China has also fueled our recovery. The world is counting on them to pull us out of this recession. They are battling inflation and they are committed to winning that war. China has increased interest rates six times this year and it has raised bank reserve requirements six times this year. Officials stated last week that they will remain vigilant even though economic activity is contracting. This could be one of the biggest market threats during the next few months.

European credit concerns are alive and well. Greece is still waiting for confirmation that it will get the bailout money it needs. That process could take another six weeks and the market will be "holding its breath". The EU can't solve this little problem, what will it do when Italy and Spain come knocking? The new credit facility won’t be ramped up until late in 2011 because they have not been able to agree on bailout terms. Interest rates in Spain and Italy are climbing and they are within striking distance of 6.5% on the 10-year. Historically, once rates rise above this level, "the genie is out of the bottle".

If you took my advice, you are long puts and you are making great money. I have not gone overboard with these positions because we could see a relief rally when the debt ceiling gets raised. During the next few days, I expect the various plans to be batted back and forth like a tennis ball. There will be plenty of trash talk and we will NOT get a solution before the open Monday. The market will tank and I will take profits when I see an air pocket.

The money I can make in this scenario is much greater than the losses I would sustain if Washington pulls a rabbit out of its hat. I am willing to take this bet, but I am keeping my size relatively small.

The relief rally will be fairly short-lived. When it stalls, it will set up an excellent shorting opportunity and then I will buy puts in size. All of the other factors I mentioned above will come into focus once the dust settles.

After yesterday's dramatic decline, I would expect a bounce this morning. The House will approve Boehner’s plan and that will spark some optimism until it gets shot down in the Senate. If bulls can’t add to early gains, the market will drift lower this afternoon. GDP could be a small positive for the market tomorrow. It has come in high and it has been revised lower the last 2 quarters. Friday will be flat and all eyes will be on Washington. Traders will square up in quiet trading.

Monday, a deal will not be struck and the market will tank. Hold on to your puts and be ready to take profits. Don’t try to play the relief rally on the upside. Let it run its course and use this as an opportunity to buy (scale into) October puts.

Daily Bulletin Continues...