Resistance Is Strong At This Level – Buy Puts or Sell OTM Call Spreads!

A week ago I noticed a crack in the dam when the market was not able to rally during option expiration. The market was near a major resistance level and option open interest favored buy programs. Any small catalyst would have sparked short covering. The market seemed very tired after a huge run and it lacked a catalyst.

One way to measure momentum is to monitor the market's reaction to news events. In the past few months, the market has been able to discount economic data and buyers viewed every dip as a buying opportunity. A week ago, retail sales figures missed expectations and the market declined. Today, the market is reacting to a bigger than expected rise in initial jobless claims. In the last week, 631,000 new claims were filed and 6.7 million Americans continue to draw unemployment benefits. Bad news once again is having a negative impact on the market.

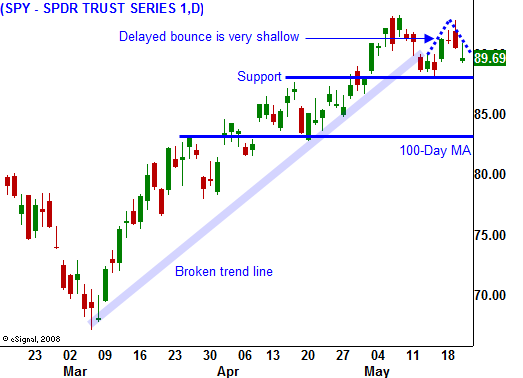

During the last two months, every dip has resulted in a snap back rally and the market consistently made new relative highs. Last week, the market drifted lower but it did not rebound. That move was rather delayed and it came Monday after the Communist Party was defeated in India's election. Democracy and capitalism are good for the market, but I was skeptical of the move. During the rally, volume was light and we hit a number of air pockets on the way up. Sellers lifted their offers and the surge had more to do with a lack of sellers than it did pent-up demand. This news was not the catalyst we needed and from what I read, the chance of a communist victory was remote.

As I've been mentioning, the market has run out of "drivers". Stimulus plans, bailouts, quantitative easing, marked-to-market rule changes, stress tests and earnings are all behind us. The market has rebounded 40% and it sits just below major resistance at SPY 94. A long-term downtrend line, horizontal resistance and the 200-day moving average converge at that price level. It will take a major event to push us through and I can’t identify the possible source.

The treasury is issuing bonds to pay for the government's $2 trillion deficit this year. As the supply of bonds hits the market, interest rates are moving higher. That will provide a stiff head wind for stocks. Companies have been issuing stock like mad and the supply of new shares is also weighing on the market.

Our budget deficit this year will be 13% of GDP, more than twice as high as it's ever been. Fortunately, it is nowhere near England's level. Their budget deficit will hit 100% of GDP this year and they face a possible downgrade from their AAA credit rating. Portugal, Spain, Greece and Ireland have already been downgraded. Governments simply can't control spending and the economic slowdown compounds the problem by reducing tax revenues.

Earnings releases will slow down dramatically next week and they are dominated by retail stocks. This sector has run up and if anything, it is priced for disappointment.

The economic calendar is full. Consumer confidence, durable goods orders, initial claims, new home sales, GDP and the Chicago PMI will be released. Now that the market momentum has slowed, weak economic news will have a negative impact. Last month, GDP missed by a large margin and dropped 6.1%. That news is likely to weigh on the market this time around if it is not revised upward.

You should be positioning itself for a pullback - “sell in May and go away”. Focus on retail, defense and REITs for your shorts. I believe the market will find support at SPY 84. Option premiums are relatively low and you can consider buying puts. If you want to play it safe, sell out of the money call credit spreads.

Daily Bulletin Continues...