The Biggest Market Threat – It’s Not the FOMC – News Pending

Posted 9:30 AM ET - The S&P 500 has been compressing in a tight range the last seven trading days. The upward momentum from the oversold bounce has stalled. Traders are waiting for major announcements this week and the outcome will determine market direction in February.

Apple posted results and iPhone sales were slightly below expectations. Service revenues were up 19% and that took some of the bite out of the announcement. The stock is up 5% and we are seeing a small relief rally. Given that the stock is near its 52-week low this is not much of a bounce. Microsoft and Facebook will post after the close and Amazon will release earnings Thursday after the close.

England's Parliament wants Theresa May to renegotiate a controversial Irish border agreement with the EU and they do not want to extend the withdrawal date. This is where the rubber meets the road. If the EU does not want to negotiate it could mean a no deal exit. Europe is very fragmented and the US has not been able to forge a trade deal. This saga will play out in the next month.

Chinese officials will resume trade negotiations in the US today. This is a high-level meeting and the statement tomorrow will have a major market impact. I suspect the tone will be friendly with few details revealed. Traders will be looking for the next scheduled negotiations. If it is more than two weeks out they will assume the negotiations are not going well.

The big news today will be the FOMC statement at 2:00 PM Eastern time. In recent weeks Fed Officials have been a little more dovish during their speaking engagements. I believe that the language will remain largely the same and they won't disclose if balance sheet reductions are planned. The press conference will be market friendly, but not over-the-top.

China's official PMI will be released tomorrow and the Caixin PMI will be posted Friday. I am expecting soft numbers. Apple and Texas Instruments cited low demand and this morning Ford said that car sales fell 54% last year (lowest since 2012). More than 23 Chinese provinces (out of 31) have reduced growth forecasts for 2019. Five rounds of easing by the PBOC have not stopped the bleeding. I believe China's economic woes are the biggest market threat this year.

Swing traders should remain in cash. We will let the last leg of this rally run its course and we will look for a shorting opportunity. I believe we could see a push to the 100-day MA and an instant reversal from that resistance. The longer we wait, the cheaper put premiums get.

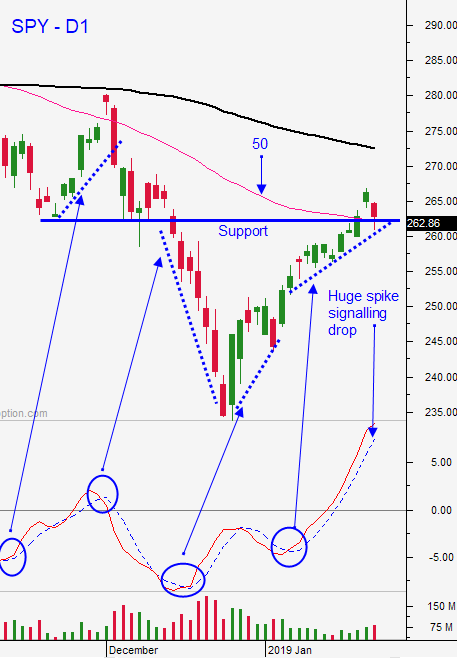

Day traders should lean on support at SPY $264. If we are above it, focus on the long side. If we are below it focus on the short side. Resistance is at SPY $267 and the next support level is $261. I suspect that we will get a nice little earnings bounce early (Boeing was excellent) and the rally will stall ahead of the FOMC. I will wait for the press conference reaction 30 minutes after the statement before I take a position. I plan to follow the momentum.

I'm expecting a little upside this morning followed by quiet trading ahead of the Fed.

.

.

Daily Bulletin Continues...