Question

I have heard people say they got a ‘good deal’ on an option price or that an option is overpriced…. what constitutes what is a ‘good deal’ or what is overpriced?

Answer

Great question!

Many traders associate a “good deal” with a winning trade, but that doesn’t necessarily have to be the case. There is a difference between timing the stock and buying the option when it is “cheap”.

When you conduct your analysis and you buy a call option on a stock that has pulled back, you are getting a “good deal” on the stock. You are leveraging a long position on an asset that you believe is undervalued. This doesn’t mean that you bought the options “cheap”. The implied volatility of the options could have gone up as the stock declined.

Before you construct an option strategy, you have to evaluate the implied volatility of the options. Two distinct considerations will determine if you are getting a “good deal”.

First, you need to compare the implied volatility of the options to the historic volatility of the stock. The implied volatility of the options will indicate the market’s expected trading range for the stock. If the implied volatility is low relative to the stock’s historical price movement, you are getting a “good deal”. For example, let’s say that you can buy a three-month straddle (by a put and a call with the same strike price and the same expiration month) for eight dollars. This means that the stock needs to move eight dollars in one direction or the other in order for you to make money. If you look at a chart and the stock has a history of moving $12 in either direction during a three-month period, you are getting a “good deal”. Remember, this doesn’t mean that the stock will cooperate.

Conceivably, the market has forgotten how erratic this stock can be. If you feel that it will breakout, you will be buying the options at a bargain. Imagine a situation where the stock has fallen dramatically (30%) on a news event. The uncertainty surrounding the stock will create a huge spike in the implied volatilities. Once the stock settles down it is likely to form a base over many months. These stocks can often trade in a tight trading range while the market waits for news. As the trading range collapses, the implied volatility drops. If you buy the options, you are getting a “good deal”. However, the stock could continue to flat-line and you could lose money on the trade.

On the flipside, let’s say that the stock dropped 30% and you saw this as a dramatic overreaction to a temporary news item. As the implied volatilities spike, you could sell an out of the money put with the intention of buying the stock at a lower price. In this case, you are also getting a “good deal”. The options are relatively expensive compared to the stock’s historical trading pattern. I would caution you on this particular strategy. It is never a good idea to try and catch a falling knife. Stocks that have sharp declines usually take time to establish a support level.

I mentioned that there are two considerations that will determine if you are getting a “good deal”. The second one compares the current implied volatility to the historic implied volatility of the options. The implied volatility of the options can be charted just like the price of the underlying stock. When you view the chart, you can see how the current implied volatility compares to the 1-year range.

In the example below, you can see that BAC was trading in a tight range. The options were pricing in a relatively narrow trading range. When the stock broke support, the options were still relatively cheap. If you purchased puts, you got a “good deal”. Notice how the implied volatility increased as the stock dropped. You made money on the puts because you were on the right side of the trade and you benefited by an increase in the implied volatility.

.

.

If you are buying options when the implied volatility is near the low end of the range, you are getting a “good deal”. However, the opposite is not necessarily true. Selling the options when they are near the high end of the 52-week range may not be a “good deal”. Let’s explore both.

When the stock has gone through a “quiet period”, the Market Makers lower their expectations for the stock’s future price movement. They do so by lowering the implied volatility of the options. As a result, the options are relatively cheap and they represent a “good deal”. When you buy an option, you have limited downside risk and unlimited upside potential. You know that what you paid for the option is all that is at risk. If you were correct and the stock plunges (you bought puts), you will do very well on the trade. In the prior example, you can saw how the implied volatility of the options was at the low end of the 52-week range.

Selling options that are trading near the high end of the 52-week implied volatility range is a dangerous proposition. The price of the options did not arbitrarily increase. The Market Makers know when news is about to be released. Uncertainty translates into “expensive options”. I have seen many covered call writing scans that search out high reward situations. They simply look for high implied volatilities. Do not trust these systems, they do not account for news events.

Many novice traders will buy a stock that they are unfamiliar with and sell an at the money call with high implied volatility. They rationalize that the stock can drop 20% during the month and they will still breakeven. On the upside, the stock can stay flat or rally and they will make a 20% return. Out of nowhere, the company announces that the FDA did not approve one of their drugs and the stock drops 50%. What seemed like a “good deal” was not. You need to account for material announcements. Most people don’t realize that selling naked puts (using the same strike price as the covered call you would sell) is equivalent to covered call writing. When you sell options naked, your downside risk is unlimited and your upside is capped by the premium you collected.

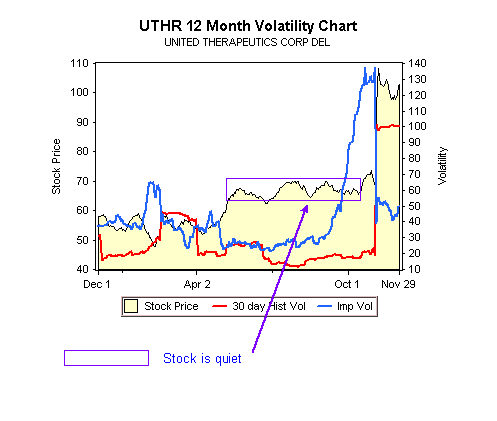

In the example below, you can see how the implied volatility for UTHR spiked even though the stock was relatively quiet. The stock was about to announce earnings and it is common for the company to disclose material events. In this case, they confirmed the efficacy of a drug that is in late stage trials. The Market Makers suspected as much and they “juiced” the options. In this case, the covered call strategy would have worked, but it was not an optimal trade. Why would you enter a position with limited upside and unlimited downside when it is surrounded by uncertainty? I have seen situations where these stocks free fall. Even buying the straddle only generated marginal returns since the options were expensive.

.

.

Uncertainty translates into higher implied volatility. The market is very efficient and it is difficult to find a “good deal”. The Market Makers are very astute and they have research teams and complex computer programs to help them price options.

I was having dinner with two colleagues that I respect and a debate broke out between them. One argued that you should only buy cheap options. The other argued that expensive options were the only ones worth buying. Both had valid points and both were correct. Spend the majority of your time researching the underlying stock. I feel that it is easier to time your trade than it is to find a “good deal”. With that in mind, you should know how the options are priced. If they are relatively cheap, look for buying strategies. If they are relatively expensive, look at selling spreads.