Introduction

In this article, we’ll delve into the art of optimizing earnings announcements using this powerful technique to help you master the world of calendar spreads and using this calendar put option strategy.

Table of Contents

Understanding Calendar Spreads

Calendar spreads are a valuable tool for options traders, leveraging the concept of accelerated time premium decay. These spreads involve buying a longer-term option while simultaneously selling a shorter-term option with the same strike price. Success in this strategy hinges on the stock remaining relatively stable, making it a classic approach. However, our Featured Trader, Dave Wyse, employs a unique twist to this traditional method.

The Options Industry Council (OIC) has free educational content. If you are not familiar with this options trading strategy, click here to learn more about it.

Leveraging Earnings with Calendar Spreads

One particularly potent application of calendar spreads is during earnings announcements. It allows traders to capitalize on the sharp decline in option implied volatility post-earnings. The uncertainty preceding the announcement causes a surge in option implied volatility for near-term options, making them more expensive than their longer-term counterparts. This, in turn, opens up opportunities.

In theory, the shorter-term option will have greater time decay than the farther-out option. Selling calendar spreads over an earnings announcement has an even bigger benefit because it capitalizes on a sharp decline in option implied volatility after the earnings announcement. The option implied volatility increases just before the earnings announcement because of uncertainty and often the option implied volatility in the near-term option is greater than the longer-term option. This creates another opportunity for us. Why would the near-term options have a higher IV?

Watch This Video to learn more about navigating Earnings Season 2024.

Retail Traders Dominate Calendar Spreads

The majority of retail traders are options buyers and they drive the price of the near-term options up. The demand for the longer-term option is not as high because the options are more expensive (on a dollar basis) and retail traders are looking for the home run (biggest percentage gain). The demand for the near-term option is higher than the demand for the longer-term option hence they are more expensive (higher IV) than the longer-term option.

Institutions Don’t Take Advantage Of This Disparity In Calendar Spreads

Institutions can’t get enough size off to make it worth while. If enough retail traders start buying calendar spreads the “edge” to this strategy will eventually narrow to the point where retail traders won’t bother with it. There is also trade management required if the stock makes a big move in this calendar put option strategy (or call).

This is not an arbitrage opportunity where the strategy will automatically work every time. Arbitrage opportunities do NOT exist for exactly this reason, institutions have already capitalized on any mis-pricing.

Interested In Learning More?

Entering Calendar Spreads

When we enter calendar spreads we are buying a call that expires a week from Friday and we are selling the call that expires this Friday. We obviously need to make sure the stock has weekly options. Since we are neutral on the stock, puts can also be used with equal efficacy, and if the stock is trading right at the strike price the put calendar spreads will be trading for the same price as the call calendar spreads. The spread will be purchased for a debit because the longer-term option is more expensive than the shorter-term option. If we exit the trade as a spread, the maximum risk is equal to the debit we paid for it.

A Practical Example

Let’s find an actual example and work through the trade. The expected move after an earnings announcement can be calculated by adding the at the money put premium to the at the money call premium. This options trading strategy is known as a straddle. If the stock was at $20 and the $20 call and the $20 put were trading for $1.50 the straddle would cost $3. If we divide the price of the straddle by the strike price we get 15% ($3/$20). In this case a 15% move is expected. In the table below you can see that the straddle is actually trading for around $3.

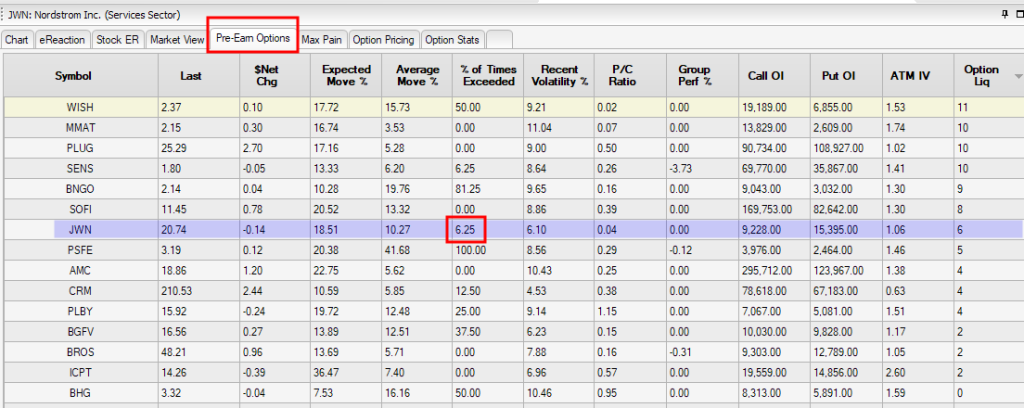

Option Stalker has calculated the expected move for stocks during the last 12 quarters and it has recorded the actual move after the earnings announcement. In the Pre-Earn Option tab, we can see the companies that announce after the close today or before the open tomorrow. We can also see the percentage of times that the stock has exceeded its expected earnings reaction in the last 12 quarters. For this calendar spreads strategy, we want stocks that rarely exceed the expected range and we want this week’s IV to be much greater than next week’s IV.

The columns of greatest interest are the Expected Move % and the % of Times Exceeded columns. In this case, we can see that the expected move for JWN is 18.51% and the % Times Exceeded for JWN is 6.25%. We want stocks that rarely make the expected move and JWN has only done that 6.25% of the time in the last three years.

Selecting the Right Stock

For this strategy to work effectively, choose stocks that historically do not exhibit significant post-earnings moves. Evaluating the daily chart is essential to pinpoint key support and resistance levels that should keep the stock within a tight range.

In this example we want JWN to stay close to the $20 strike price. If the stock rallies to $25 the $25 calls for both expirations will be deeply in the money and they will be trading for roughly the same value. The longer-term option will always trade for a slightly higher value because it expires a week later. Since the short-term call is deep in the money there is also assignment risk. If the stock is bid below parity, the assignment risk is elevated. For example, if the stock is bid $25 and the short term $20 calls are bid $4.90 they are bid below parity (they are worth $5 intrinsically).

If the short option is assigned the trader can exercise the longer-term option and exit the trade for a 100% loss. They will have effectively bought and sold the stock for $20 and they will lose the debit they paid for the calendar spread. If there is still some time premium in the option and the trader is assigned (short JWN @ $20) they can also buy the stock and sell the longer-term call option. Remember because of assignment you are short the stock and long the longer-term call. Typically, assignment will not be an issue until the Thursday before options expiration. Again, the key is to pick stocks that are likely to stay in the expected range.

In the chart below we can see that JWN has resistance at the 50-day MA and long term, horizontal support at $19. There is a very good likelihood that it will stay in that range.

Comparing Implied Volatility

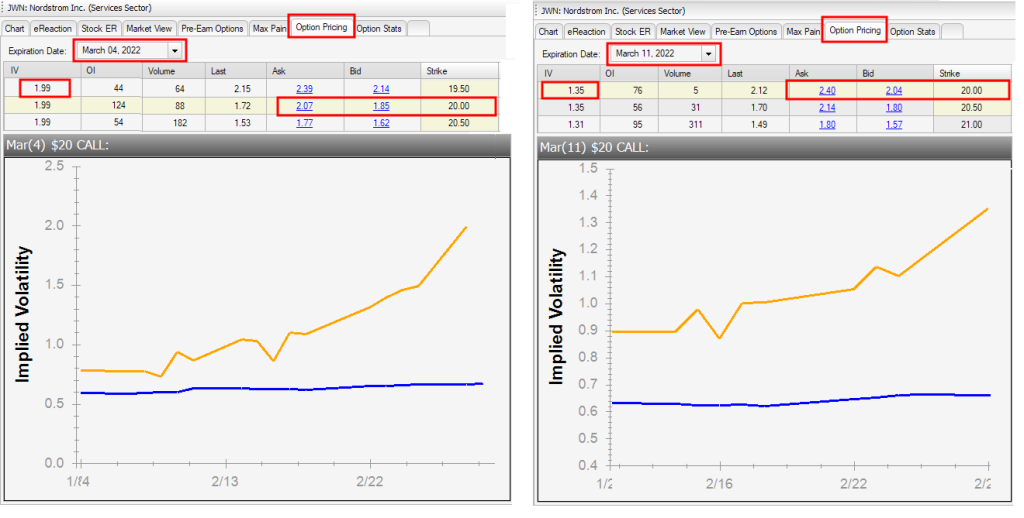

The next step is to see if the near-term options that expire on March 4th are trading at a higher IV than the options that expire a week later on March 11th. This would give us an added advantage and we would prefer this scenario. Option Stalker Pro has an Option Pricing tab. This is also based on end-of-day options data, but it is fine for these purposes.

If we click on the options price in the chain we can graphically see the change in options IV for that specific option and we can see the current value for each. In the image below you can see that the options for March 4th are trading at an IV of 1.99 and the options for March 11th are trading at an IV of 1.35. Entering calendar spreads by selling options with the higher IV and buying options with the lower IV ensures the trade will also have that “edge”.

Assessing the Trade

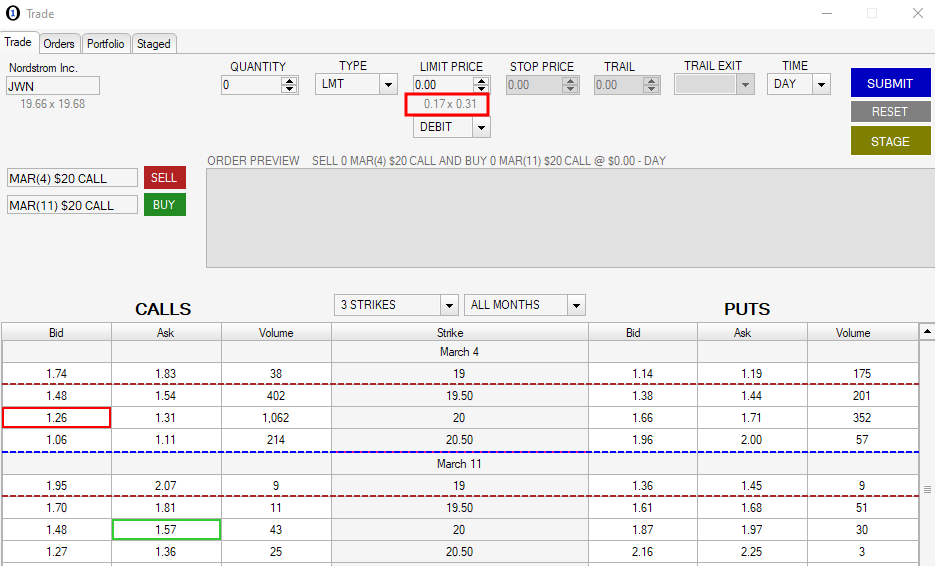

It is time to evaluate the trade. JWM has only exceeded the expected move 6.25% of the time and the daily chart suggests that it will stay in a pretty tight range because there is overhead resistance and horizontal support. The near-term options are trading at a significantly higher IV than the longer-term options. Now it’s time to look at the actual options chain.

In the image below you can see that if we buy the JWN March (11) $20 calls, and we sell the JWN March (4) calls, the spread is $.17 bid offered at $.31. Ideally, we will be able to enter the spread for a debit of $.25 which is between the bid/ask spread. Our maximum risk on the spread is $.25 and our goal is to sell it after the earnings announcement for more than $.25.

So we’ve already talked about one possible scenario where the stock rallies hard after the earnings announcement and where we have assignment risk. If we purchased a put calendar spread, the assignment risk would occur if the stock made a huge drop after the earnings announcement. We intentionally picked a boring stock so let’s look at more likely earnings reactions.

Interested In Learning More?

Exit Scenarios For Success

The morning after the release it is wise to place an order to exit the entire spread at a target profit of 20% – 40%. If the spread is placed Monday you would place a target profit of 20%. This would increase by 5% each day so that a spread that is placed Thursday you would shoot for a target profit of 40%. The closer you are to the expiration date the greater the risk and the greater the potential reward when trading calendar spreads, and all options.

In the first hour after the earnings reaction, the stock will be volatile and you should have the order working. Options prices will be all over the board and you might get a very favorable fill. If the earnings reaction is benign, you can hold the spread longer and the time decay and IV collapse on the short-term option will be greater than it is for the long-term option so you might be able to make a greater profit. This applies to this as a call spread or for a calendar put option strategy.

If we purchased the calendar spreads for $.25 and our target profit is 20%, we would place an order to sell the calendar spreads for $.30. If your target profit is 40% you would place an order to sell it for $.35.

Commissions are an important consideration for this strategy and for all trading so make sure you are using a broker with $0 commission fee schedules. This is an actual trade that is setting up and that is why I used it in this example. If you are using this strategy for more expensive stocks, the dollar gains will not seem as small.

Here’s what happens if the stock moves higher, but not dramatically. In this case the trader has the choice of legging out of the spread. In this maneuver you are buying back the short strike price and you are letting the long strike price run. The same principles as trading the underlying stock apply.

You need to make sure the market is strong and you need to wait for a bullish 1OP cross. During the most recent market dip you want the stock to preserve its relative strength. When you get the bullish 1OP cross on SPY and technical confirmation from the buy signal you buy back the short strike and you let the long strike run. For calendar spreads, when the market rally stalls or when the stock loses its relative strength you sell the long call position.

This adjustment carries added risk: Since the stock had a favorable reaction, the short calls are going to be more expensive on a dollar basis. Initially, the spread risk was only the debit ($.25). Once you buy the short strike price back, your risk increases to the price you paid for the call plus that $.25 debit. Now you are essentially trading the stock.

Make sure you have a bullish market and relative strength in the stock. If the stock has broken through technical resistance on heavy volume and you see consecutive stacked green candles with little to no overlap this could be an excellent strategy. Again, once you leg out the risk profile has changed instantly and you are speculating on the stock.

Another scenario is that the stock drops after the earnings announcement. In this case, both calls would lose value. Remember the most you can lose is the debit on the time spread ($.25). As you get closer to options expiration the options will lose their value.

The trader can close the spread down or they can buy back the short call and hold the long call. In this scenario the trader believes that the stock will rebound and they will be able to sell the longer-term call at a higher price next week. This might be a good strategy if the stock has fallen because of a drop in the market as opposed to a weak reaction to the earnings release.

If the trader believes the market and the stock will rebound this could be a sound strategy. The danger is that your long options will expire in a little more than a week and they are vulnerable to accelerated time decay so the move needs to happen quickly.

Conclusion

In conclusion, buying calendar spreads over an earnings announcement takes advantage of higher option IVs for the shorter-term options. It is important to find stocks that historically do not make big moves after earnings announcements and we can find those using the Pre-Earn Options tab in Option Stalker. This works for call calendar spreads, as we have explained in this article, or its counterpart: a calendar put option strategy.

We also need to look at the daily chart for the stock and we want to define technical support and resistance levels that should keep the stock in a tight range. The morning after the earnings announcement you should place an order to exit the spread at a pre-determined target profit between 20% and 40%. A flat earnings reaction is the best scenario.

A big rally or a big decline after the earnings announcement might require you to leg out of the spread, but that will change the risk profile of the strategy and you will be speculating the underlying stock from that point on (as opposed to trading a decline in time premium and a disparity in IV). As long as you enter and exit the position as a spread your risk will always be limited to the debit you paid for the calendar spreads.

Acknowledgments

A special thanks to Dave Wyse for sharing his calendar spreads calendar put option strategy.

Continue learning about Key Bars and Solos or trading Earnings Season.