Yesterday’s Market Reversal Was Impressive – Stay Long Commodity Stock Options.

Yesterday, the market staged an impressive rally. Early in the day, huge write-downs by Fannie Mae and UBS weighed on the market. The president of the National Bureau of Economic Research predicted that the US will slip into a recession. Higher oil prices also created early weakness. By midday, the market had clawed its way back to unchanged. This reversal continued right into the bell and we closed near last week's high.

This morning, the market is trading lower. Bullish markets have a tendency to establish early lows and to rally in the afternoon. That possibility exists today since the news has been relatively good.

As we have grown to expect, new home sales were very weak. However, productivity was better than expected and hourly unit labor costs declined by 2.2%. Unfortunately, work hours fell by 1.8%, representing the largest decline since 2003.

Earnings from tech giant Cisco beat expectations and the guidance was very positive. In the energy sector, DVN and RIG posted very solid numbers.

This morning, oil inventories rose more than expected and the futures are down slightly. Demand continues to outpace supply and relief is nowhere in sight. Yesterday, Goldman predicted a super spike in oil prices to $150 - $200 per barrel in the next two years. I agree and we need to stay long these stocks.

There is not any news this week to drive the market. Expect choppy trading.

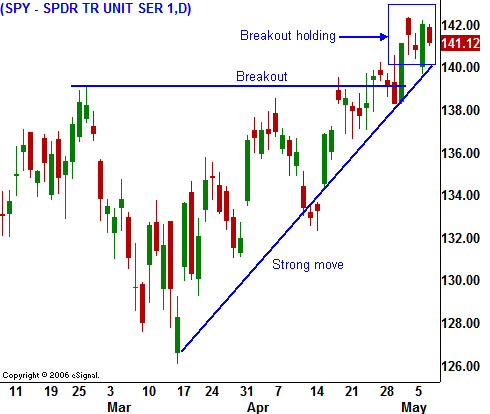

For now, stick with the short term trend and stay long commodity stocks in small size. Tech also looks like it is improving and you can selectively purchase stocks in that sector as well. If the market rallies, take profits. If the market breaks below SPY 138, exit longs and wait for a better entry point. At this juncture, I am hoping for a pullback so that I can confidently get long.

Be patient.

Daily Bulletin Continues...