Market Price Action Is Bearish – Not Likely To Improve Until Fall

Posted 9:30 AM ET - Last week we were focused on the reaction to the FOMC statement and a relief rally off of the low of the year was likely. In March the SPY started to bounce before the statement and that was a sign of pent up buying. The lack of interest into this announcement raised red flags. In March the bounce lasted 2 weeks. This time around it lasted two hours. These are signs of heavy selling pressure and I pointed them out last Friday. The S&P 500 is down 70 points before the open and the market is going to challenge the 52-week low.

Earnings have been strong. The blended growth rate for Q1 S&P 500 EPS is 9.1% (4.7% expected). Of the 87% of S&P 500 companies that have reported for Q1, 79% have beaten consensus EPS expectations (above the five-year average of 77%). In addition, 74% have surpassed consensus sales expectations (above the five-year average of 69%). So what gives, why is the market down so much? They key word in all of this is “expectations”. The market is a discounting mechanism and Asset Managers are worried about future earnings.

Higher interest rates will impact borrowing rates. This impacts corporations and consumers (home loans and credit card financing).

Inflation is running wild. Most Fed officials believe that it is temporary, but they have grossly underestimated it. Now they are hiking interest rates at a feverish pace to keep up with it and they have lost credibility. Covid-19 in China (340 container ships off the Shanghai port), the war in Ukraine and droughts are not helping inflation concerns.

China has been the global growth engine for the last two decades. It is the second largest economy in the world and hyper growth leads to “excess”. I sense that a major bubble in China and if I am right, it will have a massive ripple effect. The warnings signs have been there for well over a year and their market has been in a steady down trend. That is a sign that money is leaving.

Last week we saw very soft PMI numbers in China. This morning they reported that exports grew 3.9% (Y/Y) and imports were flat (Y/Y). These are the lowest levels in 2 years. China premier Li Keqiang warned of a 'grave' jobs situation. Bloomberg reported new China home sales fell 33% over holiday period in 23 major cities. Property developers in China are defaulting on bond payments and credit concerns are surfacing. Investors do not know to what extent (if any) the PBOC will back these companies. On Friday, Taiwan's air force was scrambled to warn away 18 Chinese aircraft that had entered its air defense zone, with further incursions on Saturday and Sunday. China is supporting Russia’s war efforts and this could impact global trade relations.

In the US, domestic job growth was strong last week. This will help the market, but if that number starts to drop we will see a swift round of selling. Even a robust jobs number Friday did not keep sellers at bay.

An unintended consequence of low interest rates is that investors are pushed out on the risk curve. They have to own stocks because they can’t generate a return in fixed income. Bond yields are producing negative real returns and they do not keep pace with inflation. “Baby boomers” are retiring and they can’t shoulder risk like they were able to 15 years ago. Their earning years are behind them and now they are trying to hang on to what they have. Scared money never wins and these are weak hands. When the market is going up no one is worried. However, once the market corrects (10% drop) they will get very nervous. The SPY is close to a 10% correction ($390).

My comments are lengthy today because I want you to be aware of the dark clouds. I do not see them parting for many months and the impact of Fed tightening will not be known until the fall and another 50 basis point hike is likely in a few weeks.

As short term traders, we just follow price action. The price action points lower and the selling pressure is heavy.

Nimble swing traders can take overnight shorts, but do not overstay your welcome. The market has violent snap back rallies. Longer term swing traders with a 3-4 week time frame should stay sidelined. If we see a deep drop and a capitulation low, there will be an opportunity to sell bullish put spreads. I will let you know if that sets up.

Day traders should have a bearish bias heading into each day. There is no reason to chase stocks in either direction. This volatility provides plenty of opportunities to get long or short. The advantage to trading the short side is that you will have a market tailwind. If a position is working out particularly well, you have the latitude to hold some of it overnight if you are short. You do not have that when you are playing the long side. We are making a big gap down this morning to a new low for 2022. Horizontal support levels will fail instantly and I believe we will see a gradual drift lower in the first 90 minutes and then we will compress on the low of the day. The chance of a bullish gap reversal is low and any bounce will provide an excellent shorting opportunity.

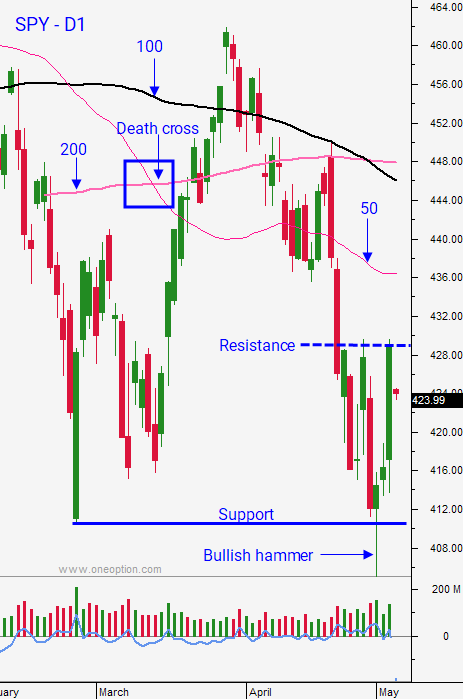

Support is at SPY $405 and $400. Resistance is at $407.50 and $415.

.

.

Daily Bulletin Continues...