Market Pricing In Positive Outcomes – Surprise Favors Downside

Posted 9:30 AM ET - Yesterday the market showed signs of strain. The FOMC minutes were dovish and US/China trade negotiations cleared a major hurdle. Stocks initially surged on the news and then drifted lower. This is a major warning sign.

Today we will get more "Fed Speak", but don't expect anything new. The balance sheet "roll-off" should end early next year. Based on projected economic growth the Fed still expects at least one more rate hike this year. The market is not pricing in rate hikes so any surprise favors the downside.

President Trump will meet with the lead negotiator from China at 2:30 PM ET today. Trade negotiations have gone so well that both sides wanted to continue through the weekend. In all likelihood Trump will extend the March 1st deadline. This news is largely priced into the market and a deal is expected.

Trade negotiations with the EU are at a standstill. The European Trade Commission will meet today to discuss a blueprint for a Trans-Atlantic deal. Officials are hoping that an agreement can be reached by the end of the year. Trump will get impatient and he will set an earlier deadline. The EU is very fragmented and the negotiations will drag on as they did with England.

Brexit is only 40 days away and the chances of a hard exit are increasing. Parliament voted not to extend the deadline and Europe is not budging on the Irish border issues. A train wreck is possible.

Global economic conditions are deteriorating. The third and fourth largest economies in the world (Japan and Germany respectively) posted weak flash PMI numbers. Next Thursday China will post its official PMI and the EU will release its official PMI.

Domestic conditions could be faltering. Last week retail sales declined a surprising 1.3%. Durable goods orders were lower than expected and the Philly Fed was also soft yesterday. GDP will be released next week and traders are fearful that the global soft patch might be spreading to the US. I believe this is the greatest threat to the market rally and it is not priced in. With each economic release the selling pressure will build.

Earnings season has ended on a positive note. Profits hit record levels and stocks are trading at the upper end of their valuation range.

Momentum drives the market lower than it should go and it fuels it higher than it should go. I believe the current rally is over-extended and that we are due for a pullback. There are many unresolved issues and the market is pricing in positive outcomes.

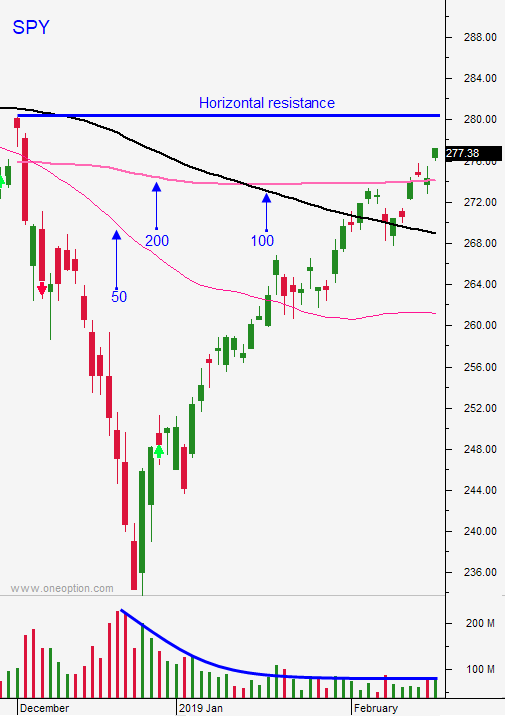

Swing traders should remain in cash until the SPY trades below $274. When that happens, short the market and use SPY $281 as a stop on a closing basis. We will give the trade room to move. As the market trends lower we will adjust our stop.

Day traders should watch the first hour range. If the market is trapped in the range, fade the extremes. If the market breaks out of the first hour range, favor that side as long as it remains outside of the first hour range. Trading volume has been light and you can see a compression forming on the daily chart. This means you have to reduce your size and activity. Support is at SPY 276.25 and resistance is at SPY $278.75.

There is a chance for a market rally this afternoon when Trump extends China's deadline. This is largely expected and I would only buy if the market is near the low of the day heading into the 2:30 PM ET meeting. Traders were not overly excited by the US/China trade developments yesterday and the reaction could be muted.

Major economic releases next week should dampen spirits and soften the bid.

.

.

Daily Bulletin Continues...