Market Speed Bump Ahead – Watch Out For This News

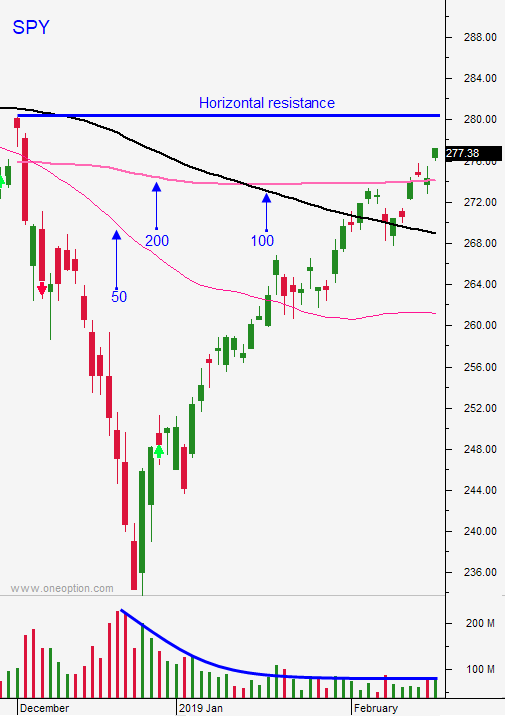

Posted 9:30 AM ET - The market has been showing signs of strain. The last two days we have seen late day selling and follow through the next morning. Horizontal resistance at SPY $281 is stiff and a major round of economic releases tomorrow could spark selling.

US/China trade negotiations are going well and a deal is fully priced into the market. Any surprise favors the downside.

Theresa May is trying to extend the Brexit deadline, but her own Parliament voted not to a month ago. She has also tried to get additional concessions from the EU and they are not budging. The next vote is scheduled on March 12th and that is only 17 days from the deadline. This certainly feels like a train wreck and it will come down to the wire. Investors hate uncertainty and this is a dark cloud. Manufacturers are moving production/inventory out of England and central banks are preparing to backstop trillions of dollars in derivatives.

Global economic conditions are soft. Japan and Germany (third and fourth largest economies in the world respectively) posted weak flash PMI's a week ago. Tomorrow the official PMI's will be released and they will include China (no flash PMI reported). China's economy has been slipping and retail sales dropped 4.4% during their busiest time of year (Chinese New Year). The PBOC has been easing to no avail. I believe these releases will weigh on the market.

Yesterday, Fed Chairman Powell testified before Congress and he said that global economic conditions are deteriorating. That is the primary reason the Fed has softened its policy. The yield curve is flattening and that suggests a possible recession later in the year. The market is not pricing in any rate hikes, but most Fed officials expect at least one more hike this year. Any surprise favors the downside.

Domestic economic activity is showing signs of strain. Retail sales, durable goods orders and the Philly Fed all missed expectations. Tomorrow we will get the advanced (first) reading for Q4 GDP. Analysts are expecting 2.3% growth. Chicago PMI will also be released. Any weakness will spark selling. At these lofty levels I doubt that in line numbers will attract buyers. It would take exceptional numbers to fuel a rally and given the recent trend, that is unlikely.

Earnings season has ended and the results were fantastic. At a forward P/E of 16, stocks are trading at the upper end of their valuation range.

Trump's summit with Kim Jong-un should be light on specifics. Dialogue between the two countries will keep the relationship stable.

The market is pricing in good outcomes for all of the issues referenced above. I believe that the next sustained move is down. Swing traders should buy the SPY when it breaches $274 (200-day moving average). Use SPY $276 as your stop on a closing basis. The downside risks outweigh the upside rewards. With each economic release I believe we are closer to the drop. My concern overnight is that China could pad its numbers during the final stage of trade negotiations.

Day traders should favor the short side. The last two days the market has drifted lower after being repelled from major horizontal resistance at SPY $281. I don't see an upside catalyst and the momentum is waning. We've seen late day selling and follow through the next morning. This is a bearish pattern and we want it to continue. As long as we are below the prior day's low, favor the short side. If the market makes a new low for the day after the first hour of trading, get more aggressive with your shorts. Intraday volatility has been light so reduce your size and trade count. If we start breaking technical support levels we can increase our size.

The overnight numbers will be critical. I sense that after a 20% bounce some Asset Managers will want to lock in profits. End-of-month fund buying could offset that supply. Expect choppy trading with a downward bias. Next week we will see heavier selling if the numbers are weak.

.

.

Daily Bulletin Continues...